SNAT continued to tighten its grip on Eswatini’s Savings and Credit Cooperative (SACCO) sector in the fourth quarter of 2025, maintaining its position as the country’s largest cooperative financial institution by both assets and lending activity, according to the latest report by the Financial Services Regulatory Authority (FSRA).

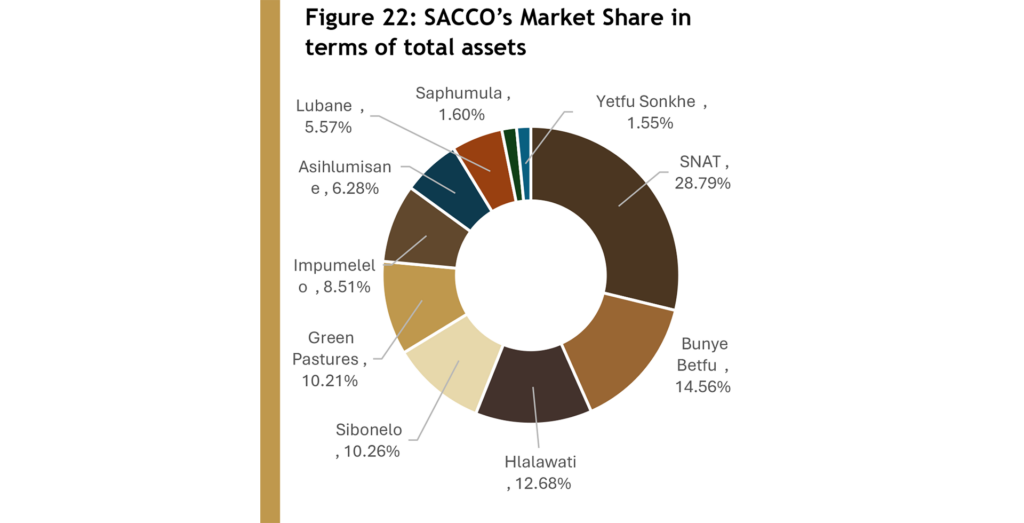

The FSRA Quarterly Statistical Report Q4 2025 shows that SNAT commanded 28.79% of the sector’s total assets among the country’s top SACCOs, reaffirming its dominance in an industry that has grown into one of the country’s key drivers of grassroots financial inclusion.

The report further reveals that SNAT also led in loans and advances, controlling 28.82% of the SACCO loan market during the review period.

The cooperative remained significantly ahead of its closest competitors, with Bunye Betfu accounting for 14.56% of sector assets, followed by Hlalawati at 12.68%. Sibonelo and Green Pastures held 10.26% and 10.21%, respectively.

In terms of lending activity, Bunye Betfu followed SNAT with a 15.23% market share of loans and advances, while Hlalawati accounted for 13.05%. Green Pastures and Sibonelo contributed 11.17% and 10.79%, respectively.

The report indicates that the dominance of the larger SACCOs continues to shape the structure of Eswatini’s cooperative finance sector, with the top five institutions collectively accounting for more than 76% of total industry assets.

This comes as the SACCO sector recorded continued growth despite prevailing economic pressures and tighter financial conditions across the region.

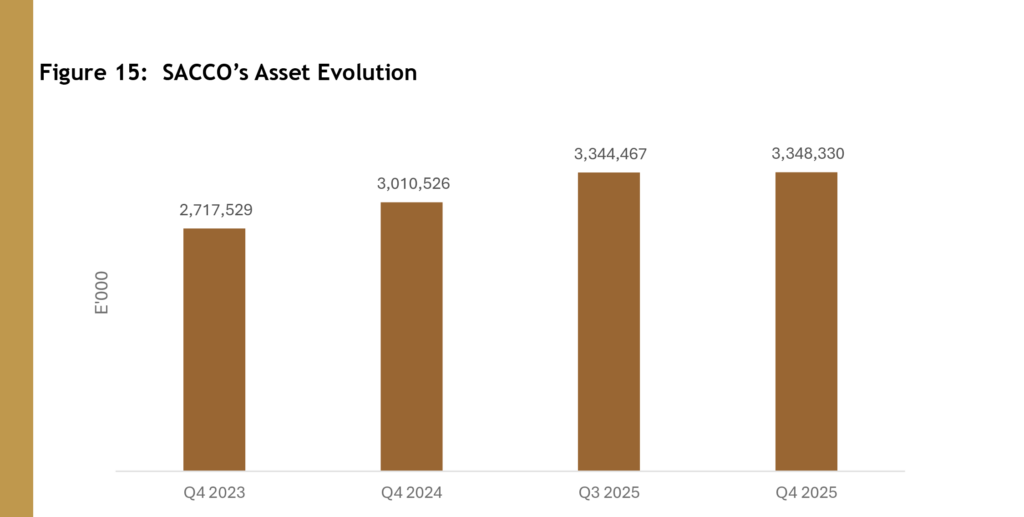

According to the FSRA, total SACCO assets reached E3.35 billion in Q4 2025, reflecting annual growth of 11.22% from E3.01 billion recorded in Q4 2024. Net loans remained the largest asset category within the sector, accounting for 71.13% of total industry assets.

The regulator noted that growth within the sector was supported by a 59.93% increase in cash and cash equivalents, a 67.49% rise in prepayments and sundry receivables, as well as continued expansion in member lending.

Loans and advances increased by 0.92% quarter-on-quarter from E2.40 billion to E2.45 billion, while year-on-year growth stood at 6.55% from E2.28 billion recorded in Q4 2024.

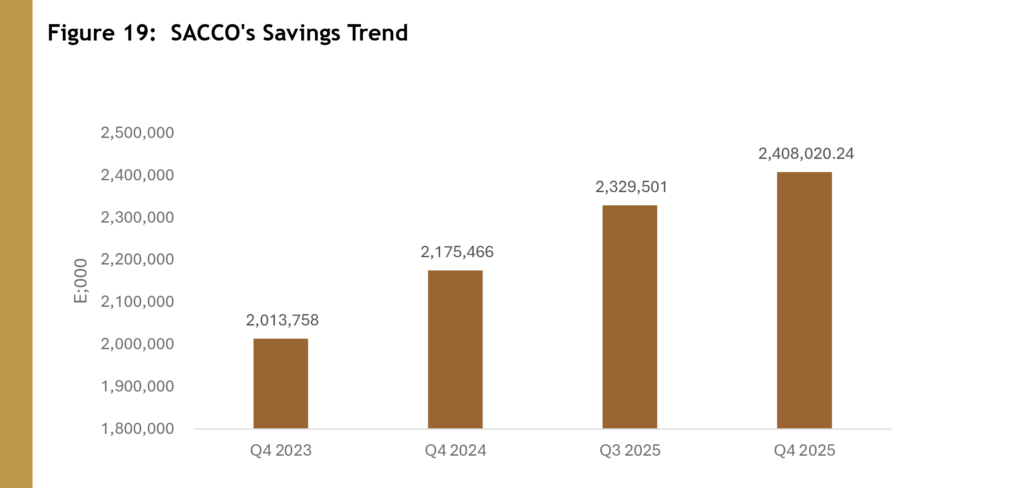

The sector also maintained strong savings momentum during the period under review, with member savings increasing by 3.37% quarter-on-quarter to E2.41 billion from E2.33 billion. On an annual basis, savings grew by 10.69% from E2.18 billion recorded in the previous year.

Meanwhile, the SACCO industry continued strengthening its financial stability indicators, with the Portfolio at Risk (PAR) ratio declining from 5.05% to 4.19% year-on-year, signalling improvements in loan repayment behaviour and credit risk management.

Institutional capital adequacy also improved to 14.7% during the quarter, remaining comfortably above the FSRA’s minimum regulatory requirement of 8%.

The report noted, however, that despite the sector’s positive overall performance, some SACCOs continue operating below mandatory capital thresholds, requiring continued regulatory oversight to safeguard long-term stability.

The SACCO sector also maintained a liquidity ratio of 10.02%, remaining within the FSRA’s prescribed limits and reflecting prudent liquidity management across the industry.