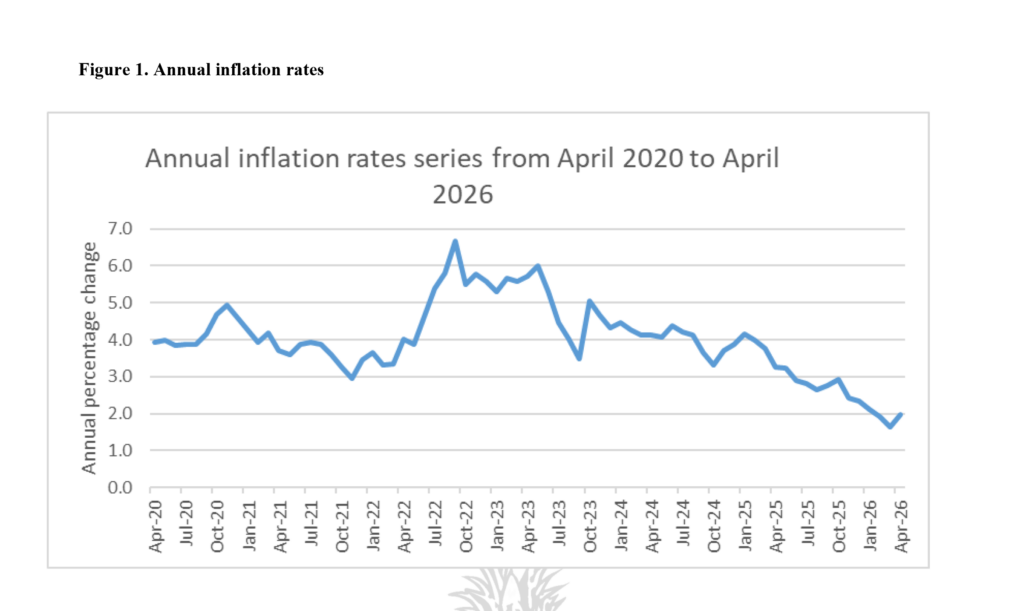

Eswatini’s annual headline inflation rate ticked upward to 2.0% in April 2026, climbing 0.33 percentage points from the 1.6% recorded in March. Despite the month-on-month acceleration, consumer price pressures remain significantly lower than the 3.3% rate witnessed in April 2025.

According to the latest Consumer Price Index (CPI) data, the upward momentum was driven by a sharp month-on-month spike in regulated utilities and energy, while the essential food basket provided crucial relief by plunging into outright deflation.

Despite this short-term acceleration, the broader macroeconomic trajectory reflects a highly cooled inflationary environment compared to last year. The 2.0% rate observed in April 2026 sits comfortably at 1.3 percentage points lower than the 3.3% headline inflation rate recorded in April 2025.

The underlying data reveals an ongoing divergence between commodity and service costs across the economy. In April 2026, the annualized inflation rate for goods stood at 2.6%, while price increases for services remained heavily subdued at 1.1%.

On a month-on-month basis, consumer prices jumped by 1.2%. This represents a significant reversal in short-term price momentum, leaping 1.3 percentage points from the deflationary -0.1% month-on-month rate witnessed in March.

The cooling of long-term price pressures across Eswatini’s economy over the past twelve months has been structurally underpinned by major relief in essential household segments, most notably within agriculture, healthcare, and retail. Leading this downward trajectory is the food and non-alcoholic beverages basket, which successfully transitioned from an inflationary print of 3.6% in April 2025 into outright deflationary territory at negative 0.9% in April 2026.

This shift has provided much-needed breathing room for household disposable income, fundamentally steered by negative growth rates in daily staples such as bread, cereals, and vegetables, alongside much softer price trajectories for dairy products, eggs, and the broader confectionery category.

Similarly, the health sector experienced a significant deceleration, dropping from 4.6% last year to a minimal 0.2% in April 2026 due to stagnant medical service fees and slower price growth for pharmaceutical products. Rounding out the annualized relief, the alcoholic beverages, tobacco, and narcotics category saw its inflation rate more than halve from 10.7% to 4.4% as a pronounced deceleration anchored wine and beer price trajectories.

In contrast to these cooling year-on-year trends, short-term price momentum from March to April 2026 was sharply accelerated by sudden, localized spikes in regulated utilities and energy products, completely reversing the flat operational costs seen earlier in the first quarter. The heavy-weight housing and utilities category broke out from a stagnant 0.0% in March to a substantial 3.9% inflation rate in April, with the upward pressure concentrated heavily in liquid fuels, domestic electricity tariffs, and water supply adjustments. Simultaneously, reflecting highly volatile global crude price adjustments, transport costs swung from negative 0.2% in March to a positive 2.4% in April, a move propelled almost entirely by the fuels and lubricants sub-category.

This energy-driven momentum naturally spilled over into the hospitality sector, where restaurant and hotel operators saw an uptick from negative 0.6% in March to a positive 1.1% in April, pushed primarily by climbing tariffs in seasonal accommodation services as Eswatini enters its peak major events and festival season.

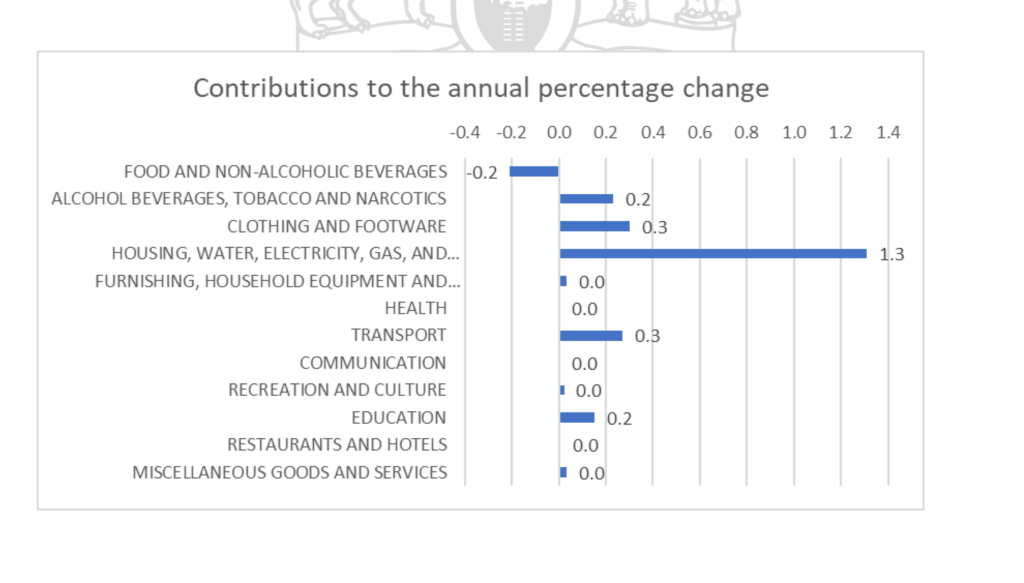

When deconstructing which of these moving pieces wielded the most mathematical influence over the final national headline inflation rate of 2.0%, three core consumption pillars accounted for virtually the entire inflationary basket. The housing and utilities sector alone contributed a commanding 1.3% to the final figure, establishing itself as the undisputed primary anchor of April’s price hikes. The remaining upward momentum was rounded out by the transport category and the clothing and footwear sector, each contributing an equal 0.3% to the national profile, effectively illustrating an economy currently caught between supply-side energy spikes and baseline agricultural relief.

The Housing and Utilities sector alone contributed a commanding 1.3% to the national rate, establishing itself as the undisputed anchor of April’s price hikes. Transport and Clothing & Footwear followed, contributing 0.3% each.