The sugar industry across the Common Market for Eastern and Southern Africa (COMESA) is a vital economic pillar that provides significant revenue and employment, though a recent regional study conducted by the COMESA Competition and Consumer Commission (CCCC) in collaboration with the Centre for Competition, Regulation and Development (CCRED) highlights that many national markets remain constrained by high costs, low yields, and heavy trade protections.

Amidst these regional challenges, Eswatini has emerged as a standout performer characterized by high productivity, excellent climate resilience, and low-cost production, serving as a benchmark for efficiency and export capability in Southern Africa. While some regional neighbours struggle with low sugar cane yields and prolonged maturity cycles, Eswatini’s sugar sector thrives on world-class agricultural efficiency.

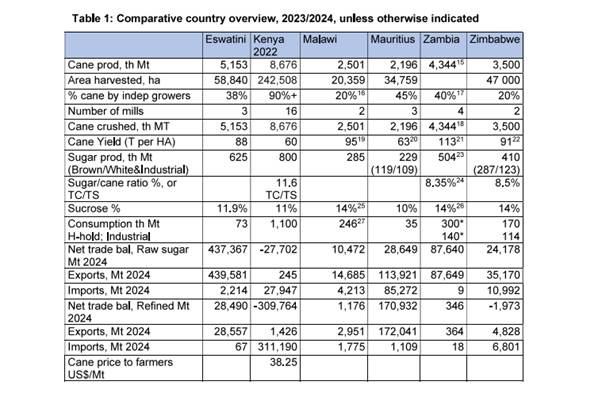

The regional study conducted by the CCCC in collaboration with the Centre for CCRED focused specifically on six countries. These countries are Eswatini, Kenya, Malawi, Mauritius, Zambia, and Zimbabwe.

Eswatini boasts an impressive sugar cane production average of approximately 5 to 6 million tonnes per annum, supported by a 100% irrigated farming model. The nation’s cane yields consistently average around 95 metric tonnes per hectare (95 Mt/h), ensuring that Eswatini, alongside Mauritius and Zambia, remains one of the lowest-cost sugar producers in the COMESA bloc. This compares exceptionally well to countries like Kenya and Mauritius, where cane yields average 60 and 63 tonnes per hectare respectively, and where farming relies primarily on rainfed models with maturity cycles stretching up to 24 months in Kenya.

According to the study, Eswatini’s exceptional production capacity enables it to readily meet domestic demand and position itself as a leading net exporter of raw sugar. The country dominates the raw sugar export market among the studied nations, leveraging robust production to access highly competitive international markets. Between 2019 and 2024, Eswatini exported more than half of its raw sugar to South Africa (54.31%), while effectively penetrating European markets, including Spain, the UK, Portugal, and Italy—and the United States.

Within the COMESA trade bloc, Eswatini also serves as a vital supply lifeline to Kenya, accounting for 8.31% of its total exports to fill the East African nation’s persistent domestic sugar deficit. A key component of Eswatini’s success is its highly structured regulatory model governed by the Sugar Act of 1967 and managed by the Eswatini Sugar Association (ESA). Unlike other regional markets where dominant millers hold unchecked bargaining power, Eswatini features a Division of Proceeds (DoP) formula that heavily incentivizes independent farmers. In Eswatini, returns are split after milling and operational costs are deducted, allocating an equitable 68.1% to growers and 31.9% to millers.

This is notably higher than the 60% share that independent growers receive in standard commercial contracts in neighbouring countries like Malawi and Zambia. Furthermore, Eswatini’s growers receive 70% of their payments upfront upon cane delivery, ensuring stable cash flow and fostering strong rural livelihoods. To encourage inclusive economic growth, the ESA also manages a dedicated revolving fund supplying crucial inputs to approximately 290 smallholder growers, ensuring that small-scale farmers are equipped to maintain high-yield and sustainable farming systems.

Despite its massive achievements, the study highlights opportunities for Eswatini to further refine its market structure to maintain its global edge. To adapt to an evolving regional market and enhance downstream competitiveness, future focus areas include modernizing historical regulatory frameworks to optimize the dual role of the ESA as both market participant and coordinator.

The study further highlights that there is also scope for introducing greater transparency regarding the value and revenue-sharing models of lucrative cane by-products such as ethanol, molasses, and co-generated electricity. Additionally, providing localized value-added packers and industrial manufacturers with more flexible supply quota allocations would help prevent local raw material shortages during peak seasons.

The strategic alignment between high-level industrial operations and regional findings was sharply underscored at the recent Standard Bank Regional Sugar Summit held at the Simunye Country Club, where Eswatini Sugar CEO Banele Nyamane framed the gathering as a vital intervention point for a sector navigating severe climate variability, rising input costs, and global price volatility. These real-time operational pressures perfectly mirror the study’s focus on the necessity for greater regional collaboration, value chain integration, and the adoptation of climate-resilient framework strategies to cushion the bloc from tightening cost environments.

Industry leaders at the summit explicitly noted that navigating the changing regional trade architecture requires moving beyond traditional production models toward sustainability-focused frameworks, directly validating the report’s recommendations regarding market diversification and the strategic modernizing of historical sector frameworks.

Further corroborating the report’s insights into Eswatini’s status as a highly efficient, low-cost regional powerhouse is the massive commitment from Associated British Foods (ABF) Sugar, whose CEO, Paul Kenward, recently lauded the Kingdom as a premier destination for long-term global capital. Backing this trust with a record £100 million investment earmarked for expansion at Ubombo Sugar Limited, Kenward highlighted Eswatini’s exceptional macroeconomic stability, reliable public-private partnerships, and transformative irrigation projects, such as the Lower Usuthu Smallholder Irrigation Project (LUSIP), as key differentiators that drive world-class yields.

Crucially, ABF Sugar’s multi-billion emalangeni development of a 40-megawatt biomass cogeneration plant to supply renewable energy to the national grid from bagasse directly answers the report’s call for the strategic commercialization of cane by-products, evidencing how corporate investment is actively turning the study’s recommendations into a profitable, climate-resilient reality.